Article

Nov 2, 2025

Banks take the drivers seat in India’s M&A Boom

Inside RBI’s bold move to fuel Corporate Deals and ignite India’s next wave of growth

The Reserve Bank of India’s October 2025 decision to allow banks to finance mergers and acquisitions marks a seismic shift in India’s corporate deal-making landscape, potentially unlocking billions in domestic capital for strategic transactions.

Overview: A Historic Policy Shift

October 2025 will be remembered as a watershed moment for India’s financial markets. The Reserve Bank of India, through its Statement on Developmental and Regulatory Policies, officially permitted commercial banks to finance corporate acquisitions for the first time in over two decades. This landmark decision, announced by Governor Sanjay Malhotra following the monetary policy committee meeting, represents far more than a routine regulatory adjustment, it’s a fundamental restructuring of how India approaches corporate finance.

Press enter or click to view image in full size

Investor confidence in the expanded revenue opportunities for lenders was evident in the immediate market response, as banking stocks soared and the Nifty Private Bank index gained almost 2% on the day of the announcement. This zeal highlights the revolutionary potential of a policy that institutionalizes acquisition financing, turning it from a specialized market dominated by private credit into a supervised, mainstream banking activity.

Impact on M&A Industry: Expanding the Total Addressable Market

India’s M&A market was already showing remarkable resilience before this policy announcement. The first half of 2025 recorded $50 billion in deal value across 1,285 transactions, with domestic deals comprising 86% of volumes. The energy sector led with $8.5 billion in deals, driven by renewable energy investments, while private equity-backed activity surged 227.6% to $5.3 billion.

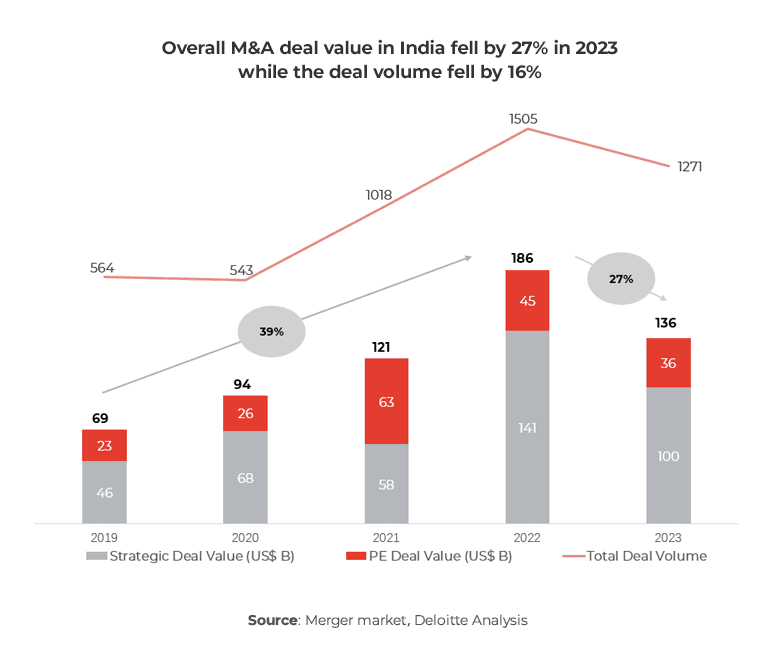

Press enter or click to view image in full size

M&A deal value and volume trends in India from 2019 to 2023 showing a recent decline in 2023 after years of growth

There is a significant expansion in the addressable market. Indian businesses mainly relied on private credit funds, NBFCs, and offshore borrowing for acquisition financing prior to this policy. In H1 2025, alternative investment funds, NBFCs, and offshore lenders financed about $9 billion worth of share transfers, while the private credit market alone deployed $9 billion across 79 deals. Banks are now entering this market, which could increase the overall financing pool by 40 to 50% and make deals that were previously unprofitable.

Infrastructure, where government policy support aligns with long-term bank lending capabilities, and technology, where consolidation plays are becoming more prevalent, are the sectors most likely to benefit. The manufacturing industry, especially export-focused businesses, could use bank connections to finance strategic acquisitions that boost their competitiveness internationally. The repercussions go beyond the volume of deals. In acquisition debt markets, market players anticipate competitive pricing structures, which could lower funding costs for reputable developers and publicly traded corporations.

Implications on Banks: Strategic Repositioning and New Capabilities

The most profound impact may be on banks themselves, forcing a strategic evolution from traditional lenders to comprehensive corporate finance partners. Large private sector banks with strong capital bases- HDFC Bank, ICICI Bank, Kotak Mahindra Bank, and Axis Bank- are positioned to lead this transformation, while public sector banks may adopt a more cautious approach initially.

Banks must now develop investment banking-style capabilities, building teams skilled in deal evaluation, valuation modeling, and cash flow projections. This evolution requires deeper collaboration with legal advisors, rating agencies, and consulting firms to assess deal quality holistically. The talent implications are significant, banks need professionals who can combine traditional credit risk analysis with sophisticated due diligence skills.

The competitive dynamics are shifting rapidly. Banks that successfully build acquisition finance capabilities could differentiate themselves in corporate relationships, while those that lag may find themselves relegated to commodity lending. The policy creates natural segmentation, with some banks evolving into full-scale corporate finance partners while others focus on retail and traditional business lending.

Importantly, banks enjoy structural advantages over private credit funds: lower cost of funds through deposits, no withholding tax complications for domestic borrowers, and existing relationships with potential acquirers. These advantages could enable banks to offer more competitive terms while maintaining healthy margins.

Why Now, Not Before? Historical Context and Current Catalysts

Understanding this policy change requires an understanding of India’s banking history. The original prohibition on acquisition financing was created in response to the financial crises of the 1990s and early 2000s, when careless lending for speculative purposes endangered banking stability. Concerns about asset-liability mismatches helped to reinforce the RBI’s prudence because bank deposits are typically short-term, while M&A loans are typically long-term.

The NPA crisis, which peaked between 2015 and 2018, further reinforced regulatory conservatism. During this period, public sector banks’ GNPA ratios rose to over 15%; some, like Indian Overseas Bank, reached 20.3%. This crisis confirmed the RBI’s cautious approach to risky lending categories.

But there has been a significant change in the landscape. Between FY2015 and FY2025, Indian banks raised almost ₹4.72 lakh crore from the markets, greatly bolstering their balance sheets. Basel III standards enhanced risk management procedures, and the Insolvency and Bankruptcy Code’s 2016 implementation produced strong resolution frameworks. Most notably, after 2018, the banking industry’s non-performing asset (NPA) ratios gradually decreased, making room for a cautious expansion into new lending categories.

The pressure to compete from private credit served as the immediate catalyst. Global funds controlled the market, with $9 billion in private credit investments in H1 2025. Banks were losing significant business relationships as a result of their incapacity to participate in a vital growth driver for their clients. In August 2025, State Bank of India formally requested regulatory relaxation, reflecting this competitive need.

Country-wise Analysis: Global Context and Best Practices

India’s action brings it closer to international banking standards because commercial banks have long funded mergers and acquisitions. Both opportunities and cautions are revealed by the global comparison.

International deal-making in the United States has been dominated by “universal banks” since the Glass-Steagall Act was repealed in 1999. Offering a broad range of financial services, from financing to strategic advisory, Bank of America and JPMorgan Chase have long been actively engaged in mergers and acquisitions. Because of this integration, U.S. banks have been able to maintain their dominance in global deal-making by offering execution speed and liquidity guarantees.

In the fiercely competitive UK market, which is regulated by the Financial Conduct Authority, both domestic and foreign banks engage in M&A activities. The UK’s emphasis on duty separation and governance to avoid conflicts of interest can be very helpful to India. European models, especially Germany’s “Hausbank” system, show that strong bank-corporate relationships can promote steady industrial growth. Within universal banking structures, German and French banks actively promote and counsel mergers that are especially advantageous to manufacturing and export-oriented industries. This model may be especially pertinent given India’s aspirations for industrial growth.

There are many lessons to be learned from Asian economies. By supporting Keiretsu and Chaebol affiliates, South Korea and Japan demonstrate how banks can play strategic roles during times of consolidation. However, emerging economies like Brazil and Indonesia have maintained more restrictive approaches, limiting bank involvement to avoid concentrated power and market destabilization.

India’s framework appears to strike a middle ground, enabling bank participation while maintaining strong regulatory oversight to prevent the pitfalls seen in other markets.

Risks and Challenges: Managing the Transition

The policy shift introduces material risks that require active management by both regulators and banks. Acquisition finance creates inherent vulnerabilities because success depends on future business synergies and extended periods for operational improvements. Failure to achieve projected synergies can lead to rapid cash flow deterioration, particularly problematic when banks hold large positions in concentrated transactions.

Concentration risk poses the most significant systemic threat. Despite the 10% Tier 1 capital limit, multiple large deals within the same industry could generate correlated losses, simultaneously impacting bank capital. The risk amplifies if underwriting standards deteriorate as banks compete for fee revenue in this new market segment.

Asset-liability mismatch presents operational challenges. Acquisition loans typically have extended repayment periods that differ from traditional corporate debt structures. Banks funding these loans through short-term deposits face increased ALM profile risks, particularly during stress periods. Legal and enforcement complexities add another layer of risk. Acquisition loans involve share pledging, SPV arrangements, and multiple security structures that complicate loan structuring.

Future Outlook: Reshaping India’s M&A Landscape

The impact of the policy will be felt gradually, with longer-term structural changes in market dynamics and short-term effects evident in deal activity. Large listed acquirers that meet eligibility requirements, especially in industries that profit from consolidation dynamics, will be the immediate beneficiaries. Transactions that were previously delayed because of a lack of domestic funding options are now possible because banks can now fund up to 70% of deal values. Changes in market structure are inevitable. Banks will create dedicated acquisition finance teams, work with NBFCs and private credit, and educate themselves on legal frameworks such as share-pledge protocols, escrow mechanisms, and SPVs in order to lower risk exposure through syndication. Market leaders will be distinguished from followers by this capability building.

The regulatory framework will likely evolve based on early implementation experience. Regulators may adjust exposure limits, risk assessment criteria, and eligibility requirements as they monitor portfolio performance in initial deals. This adaptive approach reflects the RBI’s measured liberalization philosophy.

References

Reuters. (2025, October 24). India’s RBI proposes limits for banks’ capital market exposure acquisition funding. Reuters. https://www.reuters.com/sustainability/boards-policy-regulation/indias-rbi-proposes-limits-banks-capital-market-exposure-acquisition-funding-2025-10-24/

NDTV Profit. (2025, October 26). Why RBI’s acquisition financing reform marks a structural shift in banking. NDTV Profit. https://www.ndtvprofit.com/opinion/economy-reserve-bank-of-india-rbi-acquisition-financing-reform-structural-shift-banking

EY. (2025, August 12). Navigating the M&A landscape of India: Insights of H1 2025. EY. https://www.ey.com/en_in/insights/mergers-acquisitions/navigating-the-m-a-landscape-of-india-insights-of-h1-2025

EY. (2025, August 31). How India’s H1 2025 M&A deal value held at $50.5B. EY. https://www.ey.com/en_in/newsroom/2025/08/india-s-m-a-activity-holds-ground-with-us-dollor-50-point-5-billion-in-deal-value-in-h1-2025

Bain & Company. (2024, January 29). M&A in India: Continued optimism fuels momentum. Bain & Company. https://www.bain.com/insights/india-m-and-a-report-2024/

Economic Times. (2025, October 23). RBI draft circular: Banks’ capital market exposure to be limited to 20% of Tier-1 capital. The Economic Times. https://economictimes.com/news/economy/policy/rbi-draft-circular-banks-capital-market-exposure-to-be-limited-to-20-of-tier-1-capital/articleshow/124787360.cms

Indian Express. (2025, October 24). RBI to cap bank lending for corporate takeovers at 70% of deal value. Indian Express. https://indianexpress.com/article/business/rbi-to-cap-bank-lending-for-corporate-takeovers-at-70-of-deal-value-10325040/

Business Standard. (2025, October 23). RBI proposes to allow banks to fund domestic, overseas acquisitions. Business Standard. https://www.business-standard.com/finance/news/rbi-draft-banks-funding-india-inc-acquisitions-psu-divestment-2026-125102401240_1.html

Statista. (2025, January 8). Mergers and acquisitions — India | Statista market forecast. Statista. https://www.statista.com/outlook/fmo/corporate-finance/mergers-and-acquisitions/india

IFR. (2025, October 9). M&A financing to heat up in India. IFR. https://www.ifre.com/bonds/2324149/ma-financing-to-heat-up-in-india

Financial Express. (2025, October 3). M&As: Private credit funds unfazed by entry of banks. Financial Express. https://www.financialexpress.com/business/banking-finance/mampas-private-credit-funds-unfazed-by-entry-of-banksnbsp/3997774/

EY. (2025, August 31). India’s private credit market hits US$9B H1 2025. EY. https://www.ey.com/en_in/newsroom/2025/08/private-credit-market-surges-with-record-investments-of-us-dollor-9-point-0-billion-in-h1-2025-ey-private-credit-report

Moneylife. (2025, September 30). From M&A funding to IPO financing: RBI opens door for acquisition financing by banks, expands credit flow to corporates and markets. Moneylife. https://www.moneylife.in/article/from-ma-funding-to-ipo-financing-rbi-opens-door-for-acquisition-financing-by-banks-expands-credit-flow-to-corporates-and-markets/78456.html

Economic Times. (2025, October 23). RBI draft norms say acquisition finance only for listed entities, bank exposure not to exceed 10% of Tier-1. The Economic Times. https://economictimes.com/industry/banking/finance/banking/rbi-draft-norms-say-acquisition-fin-only-for-listed-entities-bank-exposure-not-to-exceed-10-of-tier/articleshow/124788351.cms

Business Standard. (2025, October 30). RBI’s nod for banks’ M&A funding may force tweak to sensitive sector norms. Business Standard. https://www.business-standard.com/industry/banking/rbi-s-nod-for-banks-m-a-funding-may-force-tweak-to-sensitive-sector-norms-125103100805_1.html

Translink Corporate Finance. (2025, April 3). Balancing the books for cross-border M&A in India. Translink Corporate Finance. https://translinkcf.com/2025/04/04/balancing-the-books-for-cross-border-ma-in-india/

Acuity Law. (2025, October 5). Leveraged buyouts reforms: RBI’s new lending vision. Acuity Law. https://acuitylaw.co.in/leveraged-buyouts-reforms-rbis-new-lending-vision/

PwC. (2025, June 23). Global M&A industry trends: 2025 mid-year outlook. PwC. https://www.pwc.com/gx/en/services/deals/trends.html

India Briefing. (2025, May 8). India’s M&A outlook in 2025. India Briefing. https://www.india-briefing.com/news/indias-ma-outlook-in-2025-37316.html/

Nomura Connects. (2025, October 2). India M&A shows resilience in the face of tariff headwinds. Nomura Connects. https://www.nomuraconnects.com/focused-thinking-posts/india-m-a-shows-resilience-in-the-face-of-tariff-headwinds/

SNR Law. (n.d.). Financing M&A transactions in India: An overview. SNR Law. https://www.snrlaw.in/financing-ma-transactions-in-india-an-overview/

White & Case. (n.d.). Time to shine in India’s M&A market. White & Case. https://mergers.whitecase.com/highlights/time-to-shine-in-indias-ma-market

Boston Institute of Analytics. (2025, September 24). Recent mergers and acquisitions in India — August 2025. Boston Institute of Analytics. https://bostoninstituteofanalytics.org/blog/indias-biggest-mergers-acquisitions-of-august-2025-insights-for-aspiring-investment-bankers/

PwC. (2025, January 23). Tapping private credit opportunities in India. PwC. https://www.pwc.in/research-and-insights-hub/tapping-private-credit-opportunities-indias-distressed-assets-market.html

KPMG. (2025, October 16). RBI’s Octoberfest: Cheers to new regulations. KPMG. https://kpmg.com/in/en/blogs/2025/10/rbis-octoberfest-cheers-to-new-regulations.html

LinkedIn. (2025, October 5). RBI changes rules for Indian banks, shifting power in finance. LinkedIn. https://www.linkedin.com/posts/caparthverma_the-ma-game-just-changed-activity-7380813181549633536-YHG7

Economic Times. (2025, October 12). Debt capital desks may leak as banks start M&A financing. The Economic Times. https://economictimes.com/industry/banking/finance/banking/debt-capital-desks-may-leak-as-banks-start-ma-financing/articleshow/124509433.cms

Azb Partners. (2025, October 23). Unlocking offshore capital: How the RBI’s proposed ECB reforms could reshape real estate financing in India. Azb Partners. https://www.azbpartners.com/bank/unlocking-offshore-capital-how-the-rbis-proposed-ecb-reforms-could-reshape-real-estate-financing-in-india/

IIBF. (2025, August 25). SBI wants RBI’s nod for banks to finance acquisitions. LoansJagat. https://www.loansjagat.com/news/sbi-wants-rbi-s-nod-for-banks-to-finance-acquisitions

RBI. (2025, October 29). Guidelines. Reserve Bank of India. https://www.rbi.org.in/commonperson/English/Scripts/Notification.aspx?Id=900

RBI. (2024, September 23). Master circular — Exposure norms. Reserve Bank of India. https://www.rbi.org.in/commonman/english/scripts/Notification.aspx?Id=1451

ISID. (2022, July). Two phases of NPAs in India’s banks. ISID Working Papers. https://isid.org.in/wp-content/uploads/2022/07/WP240.pdf

IES. (n.d.). NPA crisis and its resolution: Focus on management. Indian Economic Service. https://www.ies.gov.in/pdfs/Nishchal-Mittal-march25.pdf

Contributors

Suvam Srivastava Dev Raj Aarit Sharma